If you own are about to purchase a home you really should understand how a mortgage works. This article is also an introduction article to a couple of future articles we have in the works.

There are five or six terms you need to understand with regard to mortgages. Two of them principal and interest apply to all mortgages. Optional items include taxes, homeowners insurance and possibly mortgage insurance. We will take a quick peek at each of them and try to provide layperson definition for each.

The down payment is the amount of money you paid towards the purchase price in cash. At the height of the real estate bubble it was not uncommon for people with good credit to not need any down payment money. In fact many of them even borrowed their closing costs. This resulted in them owing about 105% of the property value when then closed the deal.

Principal and Interest

When one buys a home they borrow a certain amount of money. This is called the principal; the amount of money you borrowed.

Interest is the fee you agree to pay each year for the privilege of borrowing the principal amount. In all standard mortgages in the US it is always paid as a percentage of the unpaid principal amount, expressed yearly but charged monthly on the unpaid principal balance. Understanding this basic concept is a key element; interest is computed on the unpaid balance you owe at the end of each month.

Optional Items

Mortgage insurance does not always apply. It is sometimes required when your down payment is not large enough for the lender to feel secure in making the loan. A third party company guarantees the difference between the amount you paid down and the amount the lender wanted. Then they charge you a fee on the principal balance until the loan is paid down to a certain level. IMO, if you can't afford the down payment, you can't afford the house. Mortgage insurance is only a decent bet for high wage earners with secure employment and no cash. Even then it is an unnecessary additional expense.

Taxes and insurance are a part of owning real estate. The lender collects 1/12th of the annual amount each month and pays the bills when they come due annually. Generally this is required unless the down payment is greater than 20% of the purchase price. The lender does not make a profit and must report payments and disbursements to you at least once per year. These expenses are not fixed and may go up or down each year depending on the amounts that need to be collected and paid.

When talking about a fixed rate mortgage without mortgage insurance only the principal amount to be paid each month and the amount of interest is a fixed amount. As the loan progresses the principal amount increases as the interest amount decreases but the monthly amount remains the same. This is how a loan is amortized, paid off.

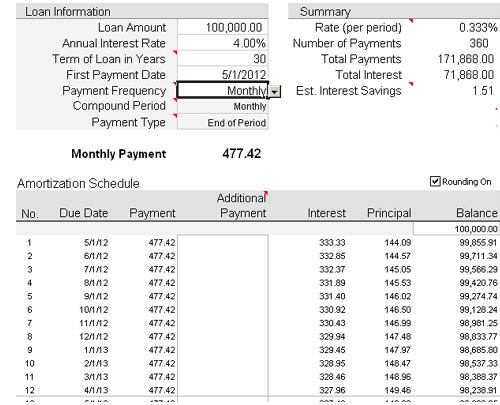

Let's take a quick look at a typical loan. We chose to use a modest amount such as one a first time home buyer would be seeking, $100,000 loan amount, the current national average interest rate of 4% and a fixed rate 30 year mortgage. This would assume a purchase price of $105-120,000 with the difference being paid in cash at closing to reduce the mortgage to an even $100,000. This would result in a principal and interest payment amount of $477.42 per month which would remain constant for 359 payments. The final month might be adjusted a few dollars either way to bring the outstanding balance to zero.

If you look at the screenshot below of the amortization schedule you will see that with your first payment only $144.09 of the 477.42 is applied to principal the rest is applied to interest. By the 12th payment that amount increases to $149.46. That process continues for the life of the loan. At about payment 153 the amounts are nearly equal and then the principal portion starts to increase more rapidly. We will revisit this in several future articles.

Edited 12-11-2012 to correct a significant typo in the last paragraph "is applied to principal the rest is applied to interest".